When you hear ACA plans, you might think of complicated forms, confusing subsidies, or maybe even political debates. But here’s the real deal: if you’re buying health insurance on your own in 2025, the Affordable Care Act is probably the reason you can even get coverage at all - and at a price you can afford.

What ACA Plans Actually Cover (No Jargon)

ACA plans don’t just give you basic care. They’re required by law to include ten essential health benefits. That means no matter which Bronze, Silver, Gold, or Platinum plan you pick, you’re getting:- Doctor visits and outpatient care

- Emergency services

- Hospital stays

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitation services (like physical therapy)

- Laboratory tests

- Preventive care (vaccines, screenings, annual checkups - often free)

- Pediatric services, including dental and vision for kids

This isn’t optional. Insurance companies can’t leave these out. That’s why, before the ACA, people with chronic conditions like diabetes or asthma got denied coverage or charged way more. Now? You can’t be turned down because of your medical history. Ever.

How Premium Tax Credits Actually Work (And Why They Matter)

Let’s say you make $50,000 a year. Before the ACA, you’d pay around $534 a month for a Silver plan on the individual market. Today, with the enhanced tax credits from the Inflation Reduction Act, you pay about $247. That’s more than $3,400 saved a year.These credits are based on your household income and the cost of the second-lowest-cost Silver plan in your area. The government pays the difference directly to your insurer. You don’t get a check - your monthly bill just drops.

But here’s the catch: those enhanced credits are set to expire at the end of 2025. If nothing changes, the average person will pay 114% more for their plan next year. For a 60-year-old in some states, premiums could jump nearly 200%. That’s not a small bump. That’s a crisis.

Medal Tiers Explained - Bronze, Silver, Gold, Platinum

The metal tiers aren’t about quality. They’re about how much you pay upfront vs. how much you pay when you use care.- Bronze (60% actuarial value): Lowest monthly premium, highest out-of-pocket costs. Best for healthy people who rarely see a doctor.

- Silver (70%): Middle ground. If you qualify for cost-sharing reductions (CSRs), this is the one to pick - your deductible and copays drop significantly.

- Gold (80%): Higher premiums, lower out-of-pocket. Good if you take regular meds or see specialists.

- Platinum (90%): Most expensive monthly, least out-of-pocket. Rarely worth it unless you have a serious chronic condition.

Most people who get subsidies go with Silver plans because they unlock extra savings. If you earn under 250% of the federal poverty level, you can get CSRs that cut your deductible in half and cap your copays. That’s huge if you need frequent care.

Who Can Get Covered? Income Rules and the Medicaid Cliff

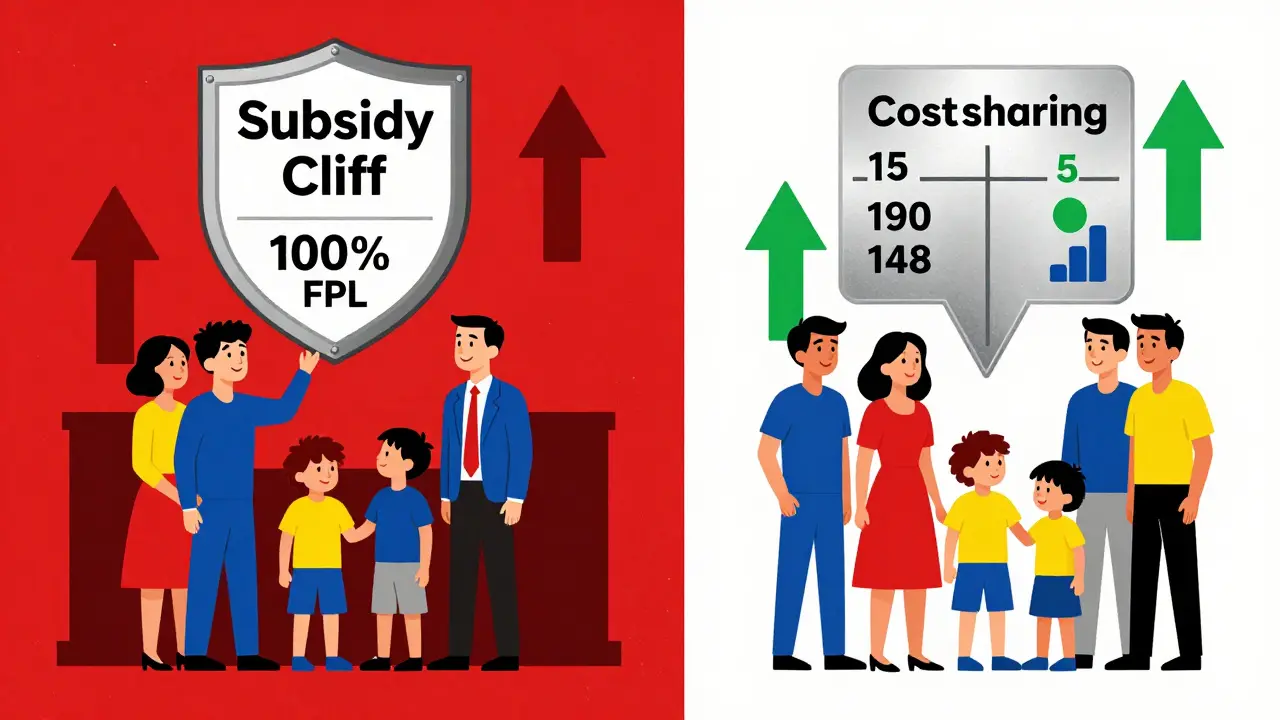

You’re eligible for premium tax credits if your income is between 100% and 400% of the federal poverty level. For a single person in 2025, that’s $15,060 to $60,240. For a family of four? $31,200 to $124,800.But here’s the problem: if you make just $1,000 over that cap, you lose everything. No credits. No help. That’s called the “subsidy cliff.” And it’s real. People have been known to turn down raises or work fewer hours just to stay under the limit.

Also, if you live in a state that didn’t expand Medicaid (like Texas, Florida, or Georgia), you’re stuck. If you make below 100% of the poverty line, you don’t qualify for Marketplace help - and you don’t qualify for Medicaid. That’s over 2 million people in 2025 with no options.

Networks, Providers, and the “Generic Coverage” Myth

Just because a plan is ACA-compliant doesn’t mean you can see any doctor. Most plans have narrow networks. That means your favorite specialist might not be in-network.Before you enroll, check if your doctors, hospitals, and pharmacies are covered. A $0 premium plan is useless if your insulin isn’t covered or your cardiologist won’t take it.

Also, “generic coverage” doesn’t mean all drugs are free. Each plan has a formulary - a list of covered medications. Some plans cover generic drugs with a $5 copay. Others make you pay full price until you hit your deductible. Always check the formulary. Don’t assume.

The Enrollment Mess - And How to Avoid It

Enrolling takes about 45 minutes. But if you’re self-employed or have variable income? You’re looking at 6-8 hours of paperwork. You need:- Your Social Security number

- Proof of income (pay stubs, tax returns, bank statements)

- Immigration documents if applicable

And here’s where most people get burned: income changes mid-year. If you make more than you estimated, you owe money at tax time. If you make less, you get a refund. But if you don’t update your income, you could end up with $2,800 in unexpected medical bills - like one Reddit user did.

Starting in 2026, you’ll have to report income changes every quarter. That’s a pain - but it’s meant to stop the tax surprises.

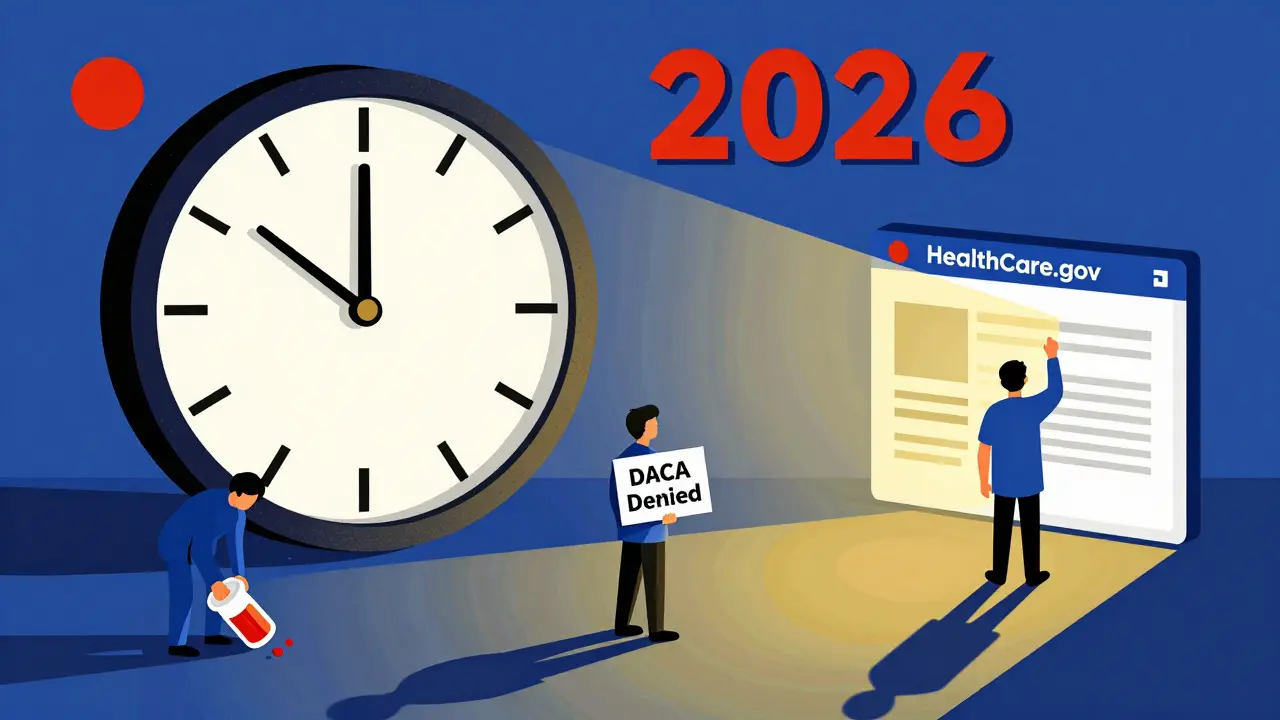

What’s Changing in 2026?

The CMS 2025 Final Rule, effective November 2025, brings big changes:- DACA recipients are no longer eligible for Marketplace coverage - about 550,000 people will lose access.

- Monthly Special Enrollment Periods for people under 150% FPL are gone. That means if you lose your job, you might have to wait months to get covered.

- Subsidies will be recalculated using 2026 IRS caps - which are much lower than the current enhanced credits.

- Insurers must use net percentage-based thresholds for payments. This sounds technical, but it means less room for error in billing.

And if Congress doesn’t act, the enhanced tax credits vanish on January 1, 2026. That could mean 3-4 million fewer people enrolled by 2027.

Who Benefits Most From ACA Plans?

- Self-employed people: No employer plan? You’re eligible for subsidies. Sarah K. from Ohio, a freelance writer earning $32,000, pays $0 for her Silver plan with full cost-sharing reductions. - People with chronic conditions: 92% of enrollees with long-term illnesses say the end of pre-existing condition exclusions saved their lives. - Young adults under 26: Can stay on a parent’s plan. No extra cost. No paperwork. - People who can’t get employer insurance: The “family glitch” fix in 2023 means if your spouse’s job offers affordable coverage for them but not for you or your kids - you can still get subsidies.What You Should Do Right Now

1. Go to HealthCare.gov - even if you think you make too much. The calculator is updated for 2026 plans. 2. Check your income estimate - if you’ve had a raise, job loss, or change in household size, update it now. 3. Compare formularies - don’t just look at premiums. Look at what your prescriptions cost. 4. Don’t wait until December - open enrollment ends December 15. If you miss it, you’re stuck until next year unless you have a qualifying life event. 5. Save your documents - you’ll need them for tax filing. If you got subsidies, you’ll get a Form 1095-A.The ACA isn’t perfect. It’s messy. It’s confusing. But for millions of Americans, it’s the only reason they have health insurance at all. If those tax credits expire, the system will fracture. And the people who lose out won’t be politicians or CEOs. They’ll be the single mom working two jobs, the freelance artist, the diabetic retiree on a fixed income.

Know your plan. Know your rights. And don’t let the noise drown out the fact: you have options. Use them before it’s too late.

Can I get an ACA plan if I have a pre-existing condition?

Yes. Under the Affordable Care Act, insurance companies cannot deny you coverage or charge you more because of any pre-existing condition - whether it’s diabetes, cancer, asthma, or even pregnancy. This protection is permanent and applies to all Marketplace plans.

What happens if my income changes during the year?

You should update your income on HealthCare.gov as soon as possible. If you make more than estimated, your subsidy may shrink and you’ll owe money at tax time. If you make less, your subsidy increases and your bills drop. Waiting until tax season can lead to large, unexpected bills - some people owe thousands. Starting in 2026, you’ll need to report changes every quarter to avoid this.

Are ACA plans cheaper than employer insurance?

Not always - but they’re often the only option for people without employer coverage. For those who qualify for subsidies, ACA plans can be significantly cheaper than buying individual insurance outside the Marketplace. However, employer plans usually have broader networks and lower out-of-pocket costs. The key difference: if your employer’s plan costs more than 9.12% of your income, you can still qualify for Marketplace subsidies.

Do ACA plans cover mental health and therapy?

Yes. All ACA plans must cover mental health and substance use disorder services as part of the essential health benefits. This includes therapy, counseling, and psychiatric care. The law requires these services to be covered at the same level as physical health services - no higher copays or stricter limits.

Can I switch plans after enrolling?

You can only switch plans during open enrollment (November 1-December 15) or if you have a qualifying life event - like getting married, having a baby, losing other coverage, or moving. If you’re unhappy with your plan outside those windows, you’ll have to wait until next year unless you qualify for a special enrollment period.

What’s the difference between Medicaid and an ACA plan?

Medicaid is government-funded health coverage for low-income people, with little to no premiums or copays. ACA plans are private insurance sold through the Marketplace, with premiums and cost-sharing. If your income is below 138% of the federal poverty level in a Medicaid expansion state, you’ll qualify for Medicaid - not a Marketplace plan. If you’re above that, you get subsidies to help pay for an ACA plan.

Comments (12)

Kathryn Featherstone

December 20, 2025 AT 00:11

I just enrolled in a Silver plan after reading this. My insulin copay dropped from $85 to $12. I didn’t even know CSRs existed until last week. Thank you for breaking it down so clearly.

Also, I updated my income on HealthCare.gov today-finally got around to it. Felt like a chore, but worth it.

Nicole Rutherford

December 20, 2025 AT 20:46

Ugh. This is why I hate the ACA. They force you into these plans then act like you should be grateful. My premiums went up 40% last year even with the ‘subsidy.’ And don’t get me started on how they cut off people who make $1 over the line. It’s a trap.

And don’t tell me ‘just get Medicaid’-I live in Texas. They don’t even expand it. So I’m stuck paying $500/month for a plan that won’t cover my neurologist.

They’re not helping. They’re controlling.

Mark Able

December 22, 2025 AT 02:02

Wait, so if I make $65k, I’m totally screwed? No help at all? I thought the cap was higher. I just got a promotion and now I’m paying full price? That’s insane.

Also, my wife’s employer plan doesn’t cover our kid-so we’re stuck with ACA. But the formulary for her asthma meds is garbage. I spent 3 hours calling pharmacies just to find one that covers albuterol at a decent price.

Why is this so hard? We’re not even poor.

Dorine Anthony

December 23, 2025 AT 21:06

Just want to say I’ve been on an ACA plan since 2020. Had a kidney stone last year. Total bill: $1,200 after insurance. Without this? I’d be in debt for years.

Also, my kid’s annual checkup was free. Vaccines? Free. It’s not perfect, but it’s the only thing keeping me sane.

Marsha Jentzsch

December 24, 2025 AT 05:41

Oh my GOD, I just realized-I’m going to lose my plan in 2026?!?!?!? I’m on a Silver plan with CSRs and I’m at 248% FPL… what if I get a 2% raise?!?!? They’re going to KILL me!!

And DACA recipients? They’re getting kicked off?!? That’s not healthcare-that’s cruelty!!

WHO’S DOING THIS?!?!? Is it the Republicans? The insurers? The government? I feel like I’m being hunted!!

I’m not even gonna sleep tonight. I’m gonna call my rep at 3 a.m. and scream.

Someone please tell me this isn’t real…

Janelle Moore

December 25, 2025 AT 09:40

ACA is a scam. The government doesn’t want you to have real choice. They want you dependent. That’s why they make it so confusing. You think you’re getting help but you’re just trapped in their system.

And those ‘subsidies’? They’re not gifts. They’re loans. You’ll pay it back later. They’re watching your income. They’re tracking you.

Also, your doctors? They’re paid by the government. You don’t own your care. You’re a number.

They’re coming for your freedom. Next they’ll control your meds. You’ll need a permit to breathe.

Henry Marcus

December 25, 2025 AT 10:06

They’re not just changing the rules-they’re rewriting the script. The CMS Final Rule? That’s not policy. That’s a power grab. The net percentage thresholds? That’s code for ‘we’re gonna screw you harder next year.’

And the Special Enrollment Periods? Gone. Why? So you can’t escape when your job vanishes. So you’re stuck. So you beg. So you cry.

They want you broken. They want you silent. They want you to think ‘I’m lucky to have this.’

Wake up. This isn’t healthcare. It’s control dressed in blue.

William Liu

December 25, 2025 AT 22:14

This is the most practical, no-BS breakdown of ACA I’ve ever read. Seriously. I’ve been avoiding this stuff for years because it felt like a maze.

But now I get it. Silver plan + CSRs = my best shot. I’m updating my income tomorrow. I’m checking my formulary. I’m not waiting until December.

Thanks for reminding me I have agency here. Even if the system’s broken, I can still make smart choices.

jessica .

December 27, 2025 AT 11:19

ACA? More like AMERICAN CRISIS. Why are we letting foreigners and illegal aliens get coverage while real Americans struggle? We spend billions on this and still people can’t get care?

And the ‘subsidy cliff’? That’s because the left wants you dependent. They want you to vote for them every time. It’s not about health-it’s about power.

Also, ‘generic coverage’? That’s just a fancy word for ‘we give you junk medicine.’

TRUMP WAS RIGHT. WE NEED TO BURN THIS SYSTEM DOWN.

Ryan van Leent

December 27, 2025 AT 12:53

Why are we even talking about this? Just get insurance through your job. If you’re self-employed, tough. You should’ve planned better. This whole ACA thing is just a bandaid on a bullet wound.

Also, who cares if your insulin costs $12? Just buy it off Amazon. I’ve seen it for $8. You’re just lazy if you can’t figure it out.

Stop whining. Get a better job. Or don’t get sick. Simple.

Sajith Shams

December 28, 2025 AT 08:33

As someone from India, I find this system absolutely insane. In my country, you pay for care directly or get it through public hospitals. No subsidies. No forms. No confusion. You just go.

Here, you need a degree in bureaucracy just to get a bandage. And you’re telling me people are crying because they might pay $300 instead of $100?

Go to a private clinic. Pay cash. It’s cheaper than this mess. I’ve seen it with my own eyes.

This isn’t healthcare. It’s a financial engineering project for lawyers and insurance CEOs.

Adrienne Dagg

December 29, 2025 AT 19:14

Just updated my income on HealthCare.gov 😌💖

My premiums dropped from $420 to $210. I’m crying happy tears. 🥹

Also, my therapist is in-network now! I’ve been going twice a week since January. This plan literally saved my mental health.

Thank you for the formulary tip. I would’ve picked the wrong plan and been stuck with $150 copays for my antidepressants 😭

YOU GUYS ARE THE BEST. 🙏❤️